The Danish Compromise revisited: implications for cross-financial sector M&A

What was once a technical corner of the Capital Requirements Regulation (CRR), suddenly found itself at the forefront of several high-profile European M&A transactions in 2025. The Danish Compromise, as the capital treatment under Article 49(1) CRR is commonly known, allows banks to risk-weight significant investments in insurance undertakings rather than deduct them from their own funds. With its application being subject to certain conditions and supervisory permission, the provision was, and to some extent still is, at the centre of a broader debate about group structures of banks, prudential consolidation and cross-sector M&A in the European Union.

Two parallel regulatory developments make the Danish Compromise particularly relevant at this moment. On the banking side, the European Banking Authority’s January 2026 Report on Consolidation (the "EBA Report") confirms a stricter reading of the Danish Compromise than anticipated by some parties, limiting the scope of the favourable capital treatment. On the insurance side, the revised Solvency II Directive appears to move in the opposite direction, introducing a similar non-deduction mechanism for insurers’ strategic participations in credit or financial institutions, potentially with a broader scope than its CRR counterpart.

Background and legal framework

Under the Basel framework, a bank’s equity and other regulatory capital investments in insurance subsidiaries are generally subject to deduction from own funds. In the CRR, this principle is reflected in Articles 36(1)(i) and 43, which provide that significant investments in financial sector entities, including insurance undertakings, must be deducted from own funds, subject to the thresholds and exceptions set out in Articles 44 to 49 CRR.

For European banking groups with material insurance operations, a model commonly referred to as "bancassurance", this deduction treatment posed a significant challenge. Full application of the deduction regime would have materially reduced group capital ratios for large bancassurance groups.

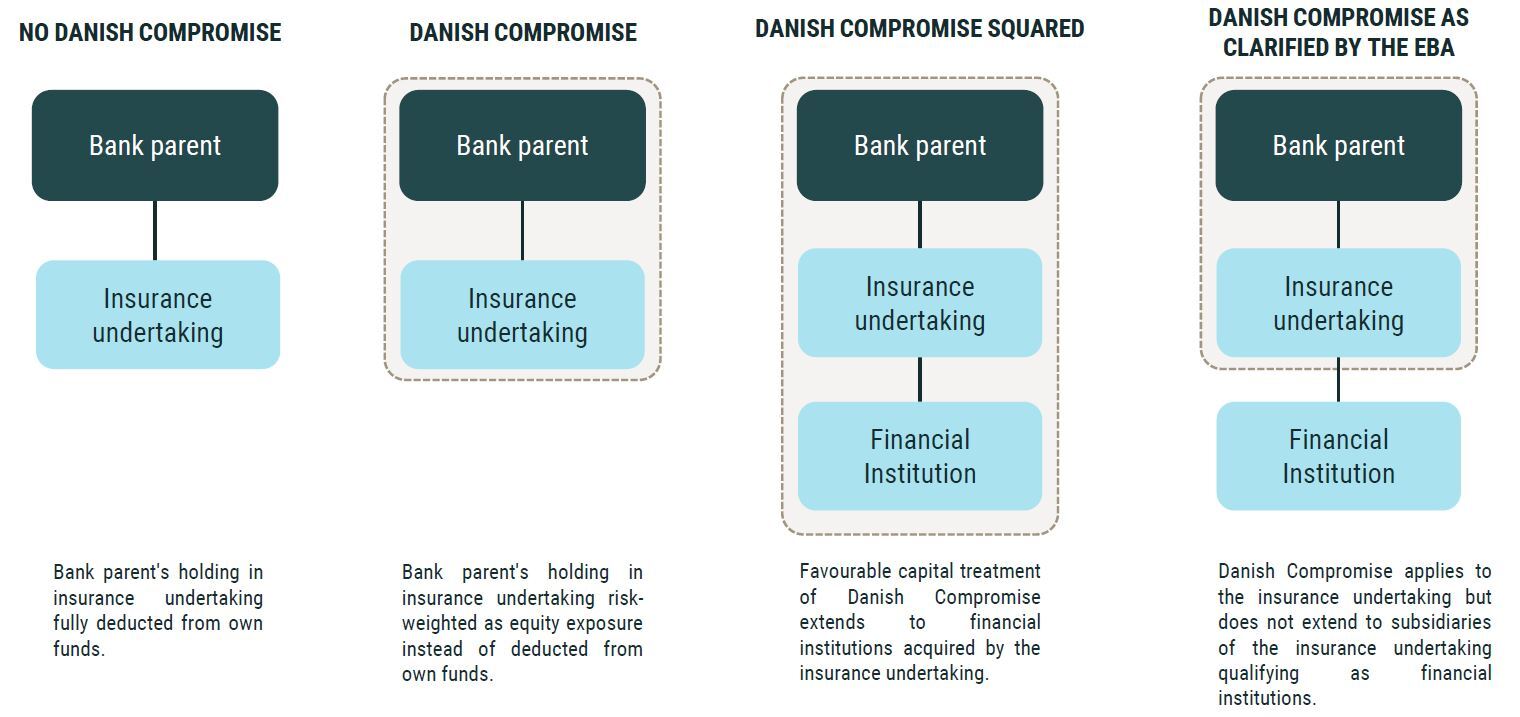

During the negotiation of the CRR in 2012, under Denmark’s rotating presidency of the Council of the EU (from which Article 49(1) CRR derives its name), a compromise was reached. France, in particular, lobbied for a more lenient approach to the capital treatment of banks' holdings of significant stakes in insurers (see here and here). The result was Article 49(1) CRR. Subject to supervisory permission, and provided that the banking group qualifies as a financial conglomerate under the Financial Conglomerates Directive, the Danish Compromise allows institutions to risk-weight their significant insurance participations as equity exposures rather than deduct them from own funds. This generally results in a lower capital burden than full deduction: a risk-weighted holding consumes only a fraction of own funds (determined by the applicable risk weight and the institution’s target capital ratio), whereas a full deduction reduces own funds euro for euro.

- For example, consider a bank with an insurance participation with a carrying value of EUR 100. Under full deduction, the entire EUR 100 would be subtracted from a bank's CET1 capital. Under the Danish Compromise, with a standard 250% risk weight, the participation generates EUR 250 of risk-weighted assets. Assuming a target CET1 ratio of 13%, the capital consumed would be EUR 32.5 (13% of 250). So the capital cost of the risk-weighted treatment would in this example be roughly one third of the capital cost under full deduction.

The "Danish Compromise squared"

In 2025, a number of transactions tested a more ambitious use of the Danish Compromise in a manner that had not previously been contemplated by supervisory and regulatory authorities. The central question was whether the favourable capital treatment under Article 49(1) CRR could extend not only to a bank’s direct investment in its insurance subsidiary, but also to assets subsequently acquired by that insurance subsidiary, in particular, asset management companies (AMCs). Market participants began referring to this extended application as the "Danish Compromise squared".

This question first came to a head in Italy. In November 2024, Banco BPM launched a tender offer of up to EUR 1.6 billion for asset manager Anima Holding. The acquisition was to be routed through Banco BPM’s insurance subsidiary, Banco BPM Vita, with the intention of applying the Danish Compromise squared. So central was this favourable capital treatment to the economics of the transaction that ECB approval of its use was included as a condition precedent in the offer documentation. In March 2025, however, the ECB communicated a negative opinion on the applicability of the Danish Compromise to the envisaged structure. Faced with the choice of abandoning the tender offer or absorbing the resulting capital impact, Banco BPM waived the condition precedent and pressed ahead, completing the acquisition in April 2025.

The Anima episode also had ripple effects on UniCredit’s concurrent all-share offer for Banco BPM itself, launched in November 2024 and valued at over EUR 10 billion. In February 2025, UniCredit issued a press release stressing that denial of the Danish Compromise would materially erode Banco BPM’s capital position and, by extension, the rationale for its offer. Although UniCredit ultimately withdrew its offer in July 2025 over so-called Italian "golden power" conditions, rather than over Banco BPM's inability to benefit from the Danish Compromise in the Anima transaction, the capital implications of the denial had coloured the entire offer process.

Finally, in August 2024, BNP Paribas announced a EUR 5.1 billion acquisition of AXA Investment Managers. The transaction was routed through BNP Paribas Cardif, the group’s insurance arm, in order to benefit from the Danish Compromise and minimise the CET1 impact. In April 2025, the ECB similarly issued a negative opinion. BNP Paribas subsequently revised the estimated CET1 impact of the transaction.

Amidst these cases, the ECB’s position on the scope of the Danish Compromise became increasingly explicit. In December 2024, Claudia Buch, Chair of the ECB Supervisory Board, indicated that the permissibility of the provision would be assessed on a case-by-case basis. By April 2025, following the negative opinions described above, she stated publicly that the Danish Compromise was intended for the insurance sector and not, for example, for AMCs.

EBA Report: scope of the Danish Compromise clarified

While the ECB's negative opinions in the cases described above provided a clear indication of the supervisory direction of travel, they did not by themselves resolve the underlying legal questions. As the ECB itself emphasized multiple times, that was ultimately a matter for EBA (or the European legislators).

On 9 January 2026, the EBA Report was published. In its final chapter, the EBA acknowledged the "interpretative challenges" arising from the supervisory review of certain M&A transactions, "particularly where financial institutions, such as AMCs, are acquired through insurance subsidiaries of banking groups", a clear reference to the transactions described above. The EBA concluded that the existing CRR framework already contained the necessary tools to address these situations, without legislative intervention.

Underpinning the EBA's analysis is a concern about regulatory arbitrage. In the EBA's view, permitting banking groups to route acquisitions of financial institutions through insurance subsidiaries in order to obtain a more favourable capital treatment or avoid deductions would risk circumventing the objectives of the prudential consolidation framework.

The "subsidiary of subsidiary" principle

The EBA’s reasoning rests on a two-step approach to prudential consolidation under Article 18 CRR. The first step is to assess the nature of the relationship between the parent undertaking that is subject to consolidation requirements and the acquired undertaking. The second is to assess the regulatory qualification of the acquired undertaking. The EBA stresses that the first step must be applied across the full chain of the parent's linked undertakings that are subject to prudential consolidation, even where an intermediate entity, such as an insurance subsidiary, is itself excluded from the prudential scope of consolidation.

The EBA places decisive weight on the definition of "subsidiary" in Article 4(1)(16) CRR, which provides that subsidiaries of subsidiaries should also be considered subsidiaries of the original parent undertaking. The EBA confirms that this is an exclusively control-based test, independent of the nature or regulatory classification of any intermediate subsidiary. Accordingly, an AMC acquired by a bank’s insurance subsidiary remains, for CRR prudential consolidation purposes, a subsidiary of the banking parent. If that subsidiary itself subsequently qualifies as a financial institution within the meaning of Article 4(1)(26) CRR, as in the AMC example considered by the EBA, it must be fully consolidated into the parent institution's consolidated situation in accordance with Articles 11 and 18 CRR.

Consolidation mechanics and capital treatment

As for the practical mechanics of consolidation, the EBA envisages a split of the carrying amount of the parent’s holding in its insurance subsidiary into two components: the portion related to the "pure" insurance business, and the portion attributable to the indirectly held financial institution (for example, the AMC). Only the former benefits from the Danish Compromise. The latter must be brought into the group’s prudential consolidation as though it were the bank’s direct subsidiary. Any goodwill or other intangible assets arising on the acquisition of the indirectly held financial institution must be recognised in the consolidated accounts of the banking parent and deducted under Article 36(1) CRR. Non-deducted assets are risk-weighted, and minority interests are treated under the ordinary CRR rules.

Relevance of prior EBA Q&A

The broader reading of the Danish Compromise – that is, the idea of a "Danish Compromise squared" – was not without regulatory foundation. In EBA Q&A 2021_6211, published in 2023, the EBA clarified that, for the purposes of Articles 36(1)(b) and 37(b) CRR, the goodwill to be deducted from CET1 in relation to a significant investment in an insurance undertaking is limited to the goodwill recognised by the investing institution when acquiring that insurance undertaking. The Q&A therefore drew a distinction between "first-level goodwill", arising when a bank acquires an insurance undertaking itself, and "second-level goodwill", arising later within the insurance undertaking – for example, where the insurer acquires another undertaking. It also confirmed that the use of the Danish Compromise does not disapply the deduction of that first-level goodwill.

This answer was read by some market participants as supporting the "Danish Compromise squared". The logic was that, if no look-through was required for goodwill generated within an unconsolidated insurance subsidiary, then any goodwill arising when that insurer acquired an AMC, for example, would likewise remain outside the scope of the bank’s own funds deduction.

The EBA Report addresses this directly. It concludes that Q&A 2021_6211 is not relevant in the context of an intermediate insurance subsidiary acquiring an entity that qualifies as a financial institution. The EBA considers that, once an indirectly held AMC is treated as a subsidiary of a subsidiary and therefore fully consolidated, the relevant goodwill is no longer goodwill on an unconsolidated insurance participation. It is, instead, goodwill recognised directly in the consolidated financial statements of the banking parent as part of the consolidation of a financial institution. On that basis, the ordinary deduction framework under the CRR applies in full.

In short, the Q&A rejected a look-through approach into an unconsolidated insurance undertaking; in the AMC scenario, according to the EBA no such look-through is needed, because the AMC, as a financial institution, falls within the prudential consolidation perimeter from the outset.

Implications for cross-sector M&A and capital structuring

The ECB’s negative opinions in the Banco BPM/Anima and BNP Paribas/AXA IM transactions, now reinforced by the EBA Report, have materially altered the economics of cross-sector M&A in the European banking sector. Industry commentators have observed that the ECB’s stance has effectively shut down a regulatory mechanism (sometimes also referred to as "loophole") that had been seen as a potential catalyst for a wave of bank-led asset management acquisitions (see here and here).

That said, this does not mean that these transactions will likely disappear entirely. It does mean that the industrial rationale will need to stand more firmly on its own merits, as the capital outcome of acquiring non-insurance financial institutions through insurance subsidiaries is less favourable than some market participants had hoped. Indeed, there still appears to be some room for capital optimisation. The EBA does not eliminate the Article 49(1) CRR treatment for the insurance participation as such; rather, it requires the carrying amount of the insurance holding to be split between the "pure" insurance business (which may still benefit from the Danish Compromise) and the portion attributable to the indirectly held financial institution (which must be fully consolidated, with any resulting goodwill deducted). That approach closes the door to the "Danish Compromise squared", but it still leaves banks room to optimise around the residual insurance component. The precise allocation between the two components may therefore become a key point of structuring attention in future transactions.

A further implication is that more creative structural responses may emerge. The focus may shift from simply placing a target under an insurance subsidiary to designing structures in which the relevant activities are genuinely carried on within an insurance-regulated perimeter – for example, through carve-outs, transfers of business lines, or mergers of activities into the insurance entity itself.

Solvency II introduction of Danish compromise for insurers

While the banking sector is facing a tightening prudential perimeter, the European insurance sector is experiencing something of a regulatory liberation. For years, insurersEuropean insurers expressed their dissatisfaction about an uneven playing field. They argued that the regulatory framework favoured bank-led conglomerates, which enjoyed capital relief when acquiring insurers, while standalone insurers faced punitive capital deductions when acquiring banking targets.

Although these concerns were arguably overstated given that Commission Delegated Regulation (EU) 2015/35 already permits non-deduction of "strategic participations" under certain conditions, the revised Solvency II Directive now enshrines that relief at the directive level, addressing this historical grievance. Revised Article 92 introduces a mechanism functionally similar to the Danish Compromise, allowing insurers to apply a more favourable capital treatment to their strategic participations, subject to conditions and prior supervisory approval.

However, the scope of this new provision creates a striking regulatory paradox. Where Article 49(1) CRR limits the favourable treatment to participations in insurance undertakings, Article 92 of the revised Solvency II Directive extends to participations in "credit or financial institutions". The irony is striking: the EBA has just ruled that the Danish Compromise does not apply to banking groups acquiring AMCs, precisely because AMCs qualify as "financial institutions". Yet under the revised Solvency II framework, insurers may well be granted capital relief for acquiring those very same financial institutions.

Concluding remarks

The EBA Report does not abolish the Danish Compromise, but it does confine it to its insurance core. That is likely to influence how cross-sector transactions will be structured and priced from now on. At the same time, the revised Solvency II Directive demonstrates that the broader debate about cross-sector transactions and prudential symmetry is far from settled. The seemingly diverging paths of the CRR and the revised Solvency II Directive highlight the complexities of regulating cross-sector financial groups.

As banks navigate stricter consolidation rules and insurers gain new M&A flexibility, the structuring of future transactions will require careful strategic planning. We would be pleased to discuss these developments in further detail and to assist with any questions that may arise. Please do not hesitate to reach out to our experts.